Retirement planning is more than just investing

PHUKET: A common question that I get from potential clients is, “Why do I need a registered investment adviser? I can buy stocks on my own.” Well, retirement planning is more than just buying and selling stocks and bonds. The answer is that retirement involves not only investment planning, but it also involves tax planning. The best way to explain this crucial point involves one of the most popular investments for yield today – master limited partnerships, or MLPs.

MLPs invest in energy assets. They’re similar to real estate investment trusts (REITs), except that they carry on an active business. This has allowed MLPs to constantly and consistently increase their payouts over the last several years. A trend which will likely continue.

There are three types of MLPs: upstream, midstream and downstream. Upstream involves exploring and developing oil and gas properties. Downstream focuses on processing and refining. Midstream refers to the companies in the middle that provide services to energy companies on either side and charge a fee for their services.

The tricky part of investing in MLPs is the way that they are taxed. An MLP pays out the income from its businesses to its owners. Income from an MLP is treated as a return of capital. MLP owners receive what is called a K-1, which is a detailed tax report showing the income and expenses of the business. Each owner is allocated a certain portion based on the number of units they own.

Because of the income MLPs generate, and the way that they are taxed, they are great for retirement, but terrible for a retirement account. What do I mean by this? By owning MLPs in your retirement account, you are actually missing out on a lot of the tax breaks you can get by owning the MLP. MLP investors not only get the income from the MLP, but they get expenses that they can write-off against all other income. This is handy for retirees looking to limit the income they have to report to Uncle Sam and lower their tax bill.

Most retirees fail to take taxes into consideration when planning for retirement. The more money they have to pay Uncle Sam, the less they have for retirement and to live on. I not only provide you with suitable investments, but I also help devise your tax plan. After all, what good is saving for retirement if the government is going to keep taking a good chunk of your money?

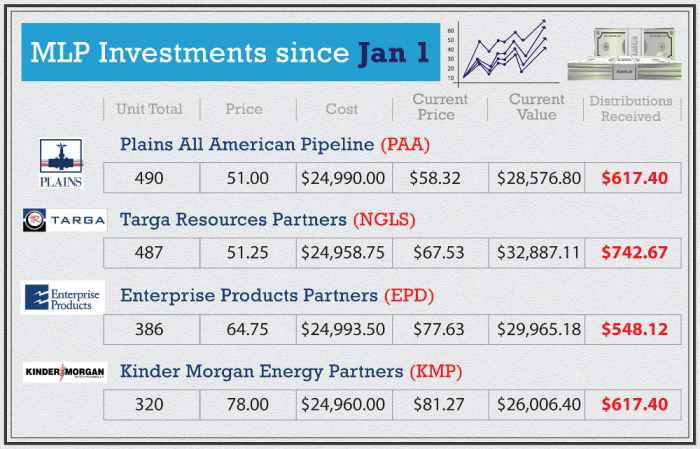

Now, let’s look and see how some MLPs have done for my clients since the start of the year. Here is how you would have fared had you put US$100,000 into these MLPs on January 1.

Not including fees, you would be sitting on US$117,435.49, good for over 17 per cent return on principal. Along the way, you would have also collected a total of US$2,791.39 in distributions. You got price appreciation and received an average yield of 5.58 per cent on your money. This is why MLPs are so attractive and why I recommend them for my clients.

Now, what are some of the risks going forward? One risk is that interest rates rise. This would increase the yield on bonds and term deposits. Investors could sell some of their MLPs and shift the money towards other assets.

What about the price of oil? The good news is that MLPs are not affected by the price of oil or natural gas, especially the pipeline MLPs like Kinder Morgan. Kinder Morgan gets paid to pipe oil and natural gas regardless of their price. Kinder Morgan charges fees based on volume, not on the price of the underlying commodity.

MLPs are great long-term investments. The increase in US oil and natural gas production will continue to drive demand for the businesses of upstream, midstream and downstream MLPs. As long as oil and gas keeps flowing, the MLPs will continue paying my clients and I and keep us happy long into our retirement here in the Land of Smiles.

Don Freeman is president of Freeman Capital Management, a Registered Investment Adviser with the US Securities Exchange Commission (SEC), based in Phuket, Thailand. He has over 15 years experience and provides personal financial planning and wealth management to expatriates. Specializing in UK and US pension transfers. Call 089-970 5795 or email: freemancapital@gmail.com.

— Don Freeman

Latest Thailand News

Follow The Thaiger on Google News: